The term ‘financial planning’ may sound unfamiliar to the common man; however, financial planning is an inherent part of a person’s life. Undeniably true, every person has had to manage money at least once in their lifetime. To manage money as efficiently as possible, people must devise a financial plan. Therefore, this article will provide anyone, regardless of prior knowledge, with a detailed understanding of how to create a personal financial plan. To learn about what a financial plan is , click here.

Note: We have moved our website to fmearticles.com; therefore, you can find this article at the following link: fmearticles.com/how-to-successfully-create-a-personal-financial-plan/

The link above is a more recently updated article that contains all the information you need to know about how to successfully devise a personal financial plan.

Note: We have moved our website to fmearticles.com; therefore, you can find this article at the following link: fmearticles.com/how-to-successfully-create-a-personal-financial-plan/

The link above is a more recently updated article that contains all the information you need to know about how to successfully devise a personal financial plan.

Components of Personal Finance

|

In personal finance, there are various significant components which are essential for one to be familiar with. The main components of personal finance are earnings, expenses, savings, investments, and tax planning. All 5 of these components are thoroughly explained below. |

|

1. Earnings

An obvious component of personal finance, earnings are the money that a person receives in return for any work done, such as a job. Any stream of income is included in this aspect.

Earnings are the foremost component because without a stream of income, it is impossible to pay expenses and meet any financial goals. Therefore, it is crucial for one to attain a steady stream of income.

Earnings are the foremost component because without a stream of income, it is impossible to pay expenses and meet any financial goals. Therefore, it is crucial for one to attain a steady stream of income.

2. Expenses

Expenses are anything that money is spent on, including both needs and wants. Some examples are food, clothing, rent, entertainment, education, travel, etc.

Due to the comprehensive list of expenses, planning out how much money will be spent will make it easier to plan for other things. If your expenses are excessive, you can prioritize them so that you can achieve your financial goals without experiencing a financial crisis.

For instance, you can purchase fewer things that aren’t vital. In this scenario, a financial plan would allow you to allot a reasonable amount of money to spend on your wants.

Another way you could reduce your expenses is by making your own food instead of buying it from restaurants.

Regardless of what your budget allows for, a financial plan will make it easier for you to record all your expenses and determine whether you need to cut expenses or not.

Due to the comprehensive list of expenses, planning out how much money will be spent will make it easier to plan for other things. If your expenses are excessive, you can prioritize them so that you can achieve your financial goals without experiencing a financial crisis.

For instance, you can purchase fewer things that aren’t vital. In this scenario, a financial plan would allow you to allot a reasonable amount of money to spend on your wants.

Another way you could reduce your expenses is by making your own food instead of buying it from restaurants.

Regardless of what your budget allows for, a financial plan will make it easier for you to record all your expenses and determine whether you need to cut expenses or not.

3. Savings

Savings mainly occur when earnings are higher than expenses, leading to surplus funds. These funds can be deposited into banks for safekeeping in the form of fixed deposits or bonds. You can utilize these funds during emergencies by withdrawing the amount you need from your bank account.

People save because savings are crucial for meeting unexpected expenditure. For instance, if your arm breaks, you’re going to have to go to the doctor to get it checked out, causing an unplanned expenditure. To cover expenditures like this, you have to save a portion of your money.

People save because savings are crucial for meeting unexpected expenditure. For instance, if your arm breaks, you’re going to have to go to the doctor to get it checked out, causing an unplanned expenditure. To cover expenditures like this, you have to save a portion of your money.

4. Investments

Investing is a method to generate more income; however, you risk losing money as well. You can invest a portion of your surplus funds in bonds, securities, mutual funds, government bonds, shares/stocks/equity, etc.

By investing, many people are able to attain more money, which they can spend, save, or reinvest. However, many people also lose money while investing, causing them to have to adjust their financial plans.

If you lose money while investing, you may have to reduce expenses or savings. However, if you reinvest all your money regardless, you will not suffer immediately. You may suffer in the long-term if you continue to lose money while investing, which will result in a failure to achieve your financial goals.

By investing, many people are able to attain more money, which they can spend, save, or reinvest. However, many people also lose money while investing, causing them to have to adjust their financial plans.

If you lose money while investing, you may have to reduce expenses or savings. However, if you reinvest all your money regardless, you will not suffer immediately. You may suffer in the long-term if you continue to lose money while investing, which will result in a failure to achieve your financial goals.

5. Tax Planning

Most families are required to pay income tax, which is determined by the government. Every country has their unique taxation laws that determine how much income tax people must pay. For instance, in the United States, you pay a predetermined percentage of your income. You can find the exact percentages here: https://www.nerdwallet.com/article/taxes/federal-income-tax-brackets

Taxes are exasperating for everyone because they make it increasingly onerous to spend, save, and invest as much as your original earnings would allow you to. However, with a financial plan, you can take action to make it easier to meet your financial goals.

For instance, you can further compromise the amount you spend on unnecessary products or you can try to increase your earnings. If neither of these options are possible, an alternative is to invest more. Although it is risky, investing may prove to be beneficial for you, allowing you to achieve your long-term financial goals.

However, it is also possible that you are not comfortable with investing a large portion of your money. Another alternative is that, with some research, you can learn which investments will provide you with tax benefits. Tax benefits allow you to legally reduce the amount of tax you pay.

Taxes are exasperating for everyone because they make it increasingly onerous to spend, save, and invest as much as your original earnings would allow you to. However, with a financial plan, you can take action to make it easier to meet your financial goals.

For instance, you can further compromise the amount you spend on unnecessary products or you can try to increase your earnings. If neither of these options are possible, an alternative is to invest more. Although it is risky, investing may prove to be beneficial for you, allowing you to achieve your long-term financial goals.

However, it is also possible that you are not comfortable with investing a large portion of your money. Another alternative is that, with some research, you can learn which investments will provide you with tax benefits. Tax benefits allow you to legally reduce the amount of tax you pay.

Factors to Consider Before Making a Financial Plan

We all need to decide about how much to spend on groceries, education, electronics, accommodation, leisure activities, etc. Furthermore, to safeguard our funds, we also make decisions regarding how much we invest and save. In other words, we make decisions every day that impact our journey to achieving our financial goals. All these decisions are affected by certain factors, which cause financial planning to vary from person to person. 3 key factors that affect financial planning are explained below.

1. Aim to Achieve

Every individual has their own financial goals. Some may want to save more, while others may want to experience as many luxuries as possible. Therefore, the amount of money that you save is dependent on your earnings, how many luxuries you’re willing to sacrifice, and your financial goals.

For instance, a college student may want to save more money than spend because of their inadequate earnings to pay for extortionate college tuition, food, shelter, transportation, etc.

Meanwhile, if you are the sole earner of a family, you will most likely have to spend more on buying a big enough house, paying for kids’ education, buying a vehicle, etc. But you still must be careful about how much you spend so that you can have sufficient money for retirement, risk coverage, emergencies, etc.

Furthermore, if you realize that your earnings are inadequate to allow you to meet your goals, learning how to invest effectively will be advantageous in getting rid of that inadequacy.

Additionally, your financial goals do not have to stay persistent; it is very likely that they change as you grow older. Don’t be hesitant to adjust your financial plan as your goals change. The purpose of a financial plan is so that you achieve your goals, and hence, stay content.

Therefore, you must ensure that your financial plan is devised in a way that allows you to accomplish your goals while experiencing the least amount of hardships possible.

Finally, your financial plan is also greatly affected by the amount you earn. If your earnings are considerably high, you will have the prerogative to purchase more freely while saving more. Remember, you can increase your earnings through strategic investing.

However, if your earnings are not as high, your financial plan will be more restricted, causing you to make wiser decisions with your money.

To sum it all, your financial plan must be devised strategically so that it allows you to successfully achieve your financial goals with as few financial complications as possible.

For instance, a college student may want to save more money than spend because of their inadequate earnings to pay for extortionate college tuition, food, shelter, transportation, etc.

Meanwhile, if you are the sole earner of a family, you will most likely have to spend more on buying a big enough house, paying for kids’ education, buying a vehicle, etc. But you still must be careful about how much you spend so that you can have sufficient money for retirement, risk coverage, emergencies, etc.

Furthermore, if you realize that your earnings are inadequate to allow you to meet your goals, learning how to invest effectively will be advantageous in getting rid of that inadequacy.

Additionally, your financial goals do not have to stay persistent; it is very likely that they change as you grow older. Don’t be hesitant to adjust your financial plan as your goals change. The purpose of a financial plan is so that you achieve your goals, and hence, stay content.

Therefore, you must ensure that your financial plan is devised in a way that allows you to accomplish your goals while experiencing the least amount of hardships possible.

Finally, your financial plan is also greatly affected by the amount you earn. If your earnings are considerably high, you will have the prerogative to purchase more freely while saving more. Remember, you can increase your earnings through strategic investing.

However, if your earnings are not as high, your financial plan will be more restricted, causing you to make wiser decisions with your money.

To sum it all, your financial plan must be devised strategically so that it allows you to successfully achieve your financial goals with as few financial complications as possible.

2. Lifestyle Choices

Everyone has their own perception of a perfect lifestyle. While many people prefer an extravagant lifestyle, many others are content with a simple lifestyle in which all necessities are fulfilled with ease.

If you are someone who desires to live extravagantly, your financial plan will be comprised of elements that allow you to spend more and save less. Contrarily, if you are content with living a life in which all necessities are effortlessly fulfilled, then your financial plan will consist of factors that require you to save more than spend.

Your lifestyle choices play a significant role in determining how money is managed in your financial plan.

If you are someone who desires to live extravagantly, your financial plan will be comprised of elements that allow you to spend more and save less. Contrarily, if you are content with living a life in which all necessities are effortlessly fulfilled, then your financial plan will consist of factors that require you to save more than spend.

Your lifestyle choices play a significant role in determining how money is managed in your financial plan.

3. Retirement

Based on the reasons, you can read through each option and choose thThe ideal age to retire varies from person to person; however, this choice makes a huge impact on your financial plan for obvious reasons.

If you plan to retire early, you must ensure that you save enough money to fulfil all your retirement wishes. Meanwhile, if you plan to retire later, you have the liberty to spend more.

However, regardless of when you choose to retire, it is imperative that you are aware of how lavishly you want to spend your retirement. If you plan on living a luxurious retirement life, then you must save more than if you were to live a simple retirement life.

Here are your options and what your financial plan should entail depending on which option you choose. Furthermore, we have also provided reasons as to why one would pick each option.

Remember, you do not need to entirely choose one option. These options are all extreme, and therefore, it is wise to alleviate the severity of these options to accommodate your preferences.

Also, note that these financial plan suggestions do not include the other factors. These suggestions are solely dependent on your retirement preferences. Furthermore, we do not know what your exact preferences are, and therefore, we can only provide reasonable estimates, not precise percentages.

If you plan to retire early, you must ensure that you save enough money to fulfil all your retirement wishes. Meanwhile, if you plan to retire later, you have the liberty to spend more.

However, regardless of when you choose to retire, it is imperative that you are aware of how lavishly you want to spend your retirement. If you plan on living a luxurious retirement life, then you must save more than if you were to live a simple retirement life.

Here are your options and what your financial plan should entail depending on which option you choose. Furthermore, we have also provided reasons as to why one would pick each option.

Remember, you do not need to entirely choose one option. These options are all extreme, and therefore, it is wise to alleviate the severity of these options to accommodate your preferences.

Also, note that these financial plan suggestions do not include the other factors. These suggestions are solely dependent on your retirement preferences. Furthermore, we do not know what your exact preferences are, and therefore, we can only provide reasonable estimates, not precise percentages.

Option 1: Retire early and live a simple retirement life.

Choosing this option will allow you to live a more relaxed life because you have to work less, and you get your needs met without conflict.

If you are someone whose ambition is to live a relaxing retirement without the need of various luxuries, then choose this option. You will be able to work for a shorter amount of time without spoiling yourself with too many luxuries.

Moreover, this option will make your financial plan consist of approximately equal spendings and savings. Nevertheless, to ensure that you are able to live your retirement life without encountering a financial conflict, it is wise to save a little more than what you spend.

When devising your financial plan, it is most logical to calculate how much money you need to save every month so that you successfully meet your retirement goals.

However, since you are retiring early and deciding to choose a simple retirement lifestyle, you will be sacrificing many luxuries.

If you are someone whose ambition is to live a relaxing retirement without the need of various luxuries, then choose this option. You will be able to work for a shorter amount of time without spoiling yourself with too many luxuries.

Moreover, this option will make your financial plan consist of approximately equal spendings and savings. Nevertheless, to ensure that you are able to live your retirement life without encountering a financial conflict, it is wise to save a little more than what you spend.

When devising your financial plan, it is most logical to calculate how much money you need to save every month so that you successfully meet your retirement goals.

However, since you are retiring early and deciding to choose a simple retirement lifestyle, you will be sacrificing many luxuries.

Option 2: Retire early but live an extravagant retirement life.

If you choose this option, you will be able to live a long and lavish retirement life because you have to work for a shorter time period, and you get most, if not all of your wishes met.

The downside of choosing this option is that your financial plan will require you to save a very large portion of your earnings, causing you to lower your spending on your wants before retirement.

This option will require you to save the most money.

This is because you are working for a shorter time period, but you also wish to enjoy luxuries. In order to successfully do this, it is intrinsic to have a substantial amount of money.

Moreover, if, when you’re almost about to retire, you suddenly decide to want to live a lavish retirement life, then it will be extremely difficult to do that.

You will instantly experience a huge burden of having to save a hefty portion of your earnings. In fact, it may even be impossible to do this if it’s only a few years before your retirement.

The reason why it’s so difficult is because you have to ensure that you have enough money till you die. Consequently, you will have to have a very large amount of money saved.

Your ability to save enough for an extravagant life depends on your earnings. However, since FME Finances thrives to provide our readers with as many opportunities and alternatives as possible, we will provide you with the best tips to switch your retirement preference.

The downside of choosing this option is that your financial plan will require you to save a very large portion of your earnings, causing you to lower your spending on your wants before retirement.

This option will require you to save the most money.

This is because you are working for a shorter time period, but you also wish to enjoy luxuries. In order to successfully do this, it is intrinsic to have a substantial amount of money.

Moreover, if, when you’re almost about to retire, you suddenly decide to want to live a lavish retirement life, then it will be extremely difficult to do that.

You will instantly experience a huge burden of having to save a hefty portion of your earnings. In fact, it may even be impossible to do this if it’s only a few years before your retirement.

The reason why it’s so difficult is because you have to ensure that you have enough money till you die. Consequently, you will have to have a very large amount of money saved.

Your ability to save enough for an extravagant life depends on your earnings. However, since FME Finances thrives to provide our readers with as many opportunities and alternatives as possible, we will provide you with the best tips to switch your retirement preference.

How to Abruptly Switch Your Retirement Preference

The best methods to apply when abruptly switching your decision from a simple to expensive retirement lifestyle is delaying your retirement, working harder to increase your earnings, or investing after retiring.

It is very likely that the first method, delaying your retirement, might not excite you if you want to retire early. Hence, the other 2 methods will allow you to retire early while being able to switch to an expensive retirement lifestyle.

FME Articles suggests that investing after retiring is the best method to keep earning more money without having to work. This will allow you to continue living the retirement lifestyle that you want.

It is very likely that the first method, delaying your retirement, might not excite you if you want to retire early. Hence, the other 2 methods will allow you to retire early while being able to switch to an expensive retirement lifestyle.

FME Articles suggests that investing after retiring is the best method to keep earning more money without having to work. This will allow you to continue living the retirement lifestyle that you want.

Option 3: Retire late but live a simple retirement life.

People who like working but dislike lavish items would choose this option. If you are someone who gets bored staying at home regardless of how many devices you possess, you will most likely want to work for a longer period of time without caring about living an extravagant retirement life.

You could also choose this option if your earnings are considerably low because you will have a consistent stream of income for a longer period of time. This income would allow you to not agonize over whether or not you meet your ends after you retire.

Choosing this option will result in a financial plan that allows you to spend more than you save. This is because you will be working for longer, and you will not need as much money after you retire, giving you the leniency of not stressing about saving as much.

This option will require you to save the least amount of money for retirement.

However, if your earnings are not enough to sustain your retirement, you may have to consider saving more than you spend. This could be difficult because meeting ends may already be a difficult task for you. Therefore, FME Finances suggests that you invest after retiring so that you continue to earn money without having to burden yourself with work.

You could also choose this option if your earnings are considerably low because you will have a consistent stream of income for a longer period of time. This income would allow you to not agonize over whether or not you meet your ends after you retire.

Choosing this option will result in a financial plan that allows you to spend more than you save. This is because you will be working for longer, and you will not need as much money after you retire, giving you the leniency of not stressing about saving as much.

This option will require you to save the least amount of money for retirement.

However, if your earnings are not enough to sustain your retirement, you may have to consider saving more than you spend. This could be difficult because meeting ends may already be a difficult task for you. Therefore, FME Finances suggests that you invest after retiring so that you continue to earn money without having to burden yourself with work.

Option 4: Retire late and live an extravagant retirement life.

This option is chosen by many people for many different reasons. The most common reason is that you want to work for a longer period of time so that you save enough money to sustain a luxurious retirement life.

Another reason as to why you may choose this option is because of the boredom you experience staying at home for long durations.

But anyways, regardless of why you choose this option, your financial plan will include aspects that will allow you to meet this financial goal of yours.

Your financial plan will require you to save less than you would if you were to retire early but still want to live an extravagant retirement life. Since you are retiring late, you will have more time to save enough money for your retirement life.

However, you will still have to save a large portion of your money. You will have to save according to how luxuriously you want to live and how much your income is.

Not knowing your exact financial goals and financial situation, a reasonable estimate is approximately equal savings and spendings (before retirement). But to ensure that you do not encounter a financial conflict in the future, it is wise to save more.

The exact amount you save depends on how late you retire and how luxurious you want your retirement life to be.

Another reason as to why you may choose this option is because of the boredom you experience staying at home for long durations.

But anyways, regardless of why you choose this option, your financial plan will include aspects that will allow you to meet this financial goal of yours.

Your financial plan will require you to save less than you would if you were to retire early but still want to live an extravagant retirement life. Since you are retiring late, you will have more time to save enough money for your retirement life.

However, you will still have to save a large portion of your money. You will have to save according to how luxuriously you want to live and how much your income is.

Not knowing your exact financial goals and financial situation, a reasonable estimate is approximately equal savings and spendings (before retirement). But to ensure that you do not encounter a financial conflict in the future, it is wise to save more.

The exact amount you save depends on how late you retire and how luxurious you want your retirement life to be.

Information About Successful Personal Financial Planning

As mentioned before, every individual has their own preferences and financial goals; therefore, a single financial plan cannot apply to everyone. Although the outline of a financial plan will always be similar, the content of the plan must be modified to accommodate all financial goals.

Moreover, as discussed in the “Aim to Achieve” section above, your age plays a significant role in your financial goals. Albeit you may have very long-term financial goals (near retirement), you will also need financial goals (goals within the next 10 years) that provide you with prosperity and a growth ladder.

When devising goals like these, you must keep your age in mind so that you do not financially struggle.

As you reach the age when you start to become completely independent, you unwillingly accept a lot of responsibility onto yourself. The biggest responsibility is keeping yourself financially stable.

These responsibilities will spontaneously originate more financial goals that will most likely be achieved within 10 years. The most common examples are buying/renting a house, financing your education, investing in acquiring additional skills that make you more inclined to getting hired, getting your own insurance, purchasing your own car, paying bills, etc.

To make it easier for you to achieve these financial goals, you must ensure that you are financially stable. Oftentimes, we may think we are financially stable; however, we do not realize that our current money habits may result in a negative impact in the far future.

You can prevent yourself from suffering in the future by making a financial plan that accounts for your current situation, financial goals, and possible future events.

Going back to how age impacts your financial goals, an elderly person’s financial plan will be specialized to support and incorporate retirement, medical bills, the decision to sell your property or distribute it among your loved ones, etc.

Moreover, as discussed in the “Aim to Achieve” section above, your age plays a significant role in your financial goals. Albeit you may have very long-term financial goals (near retirement), you will also need financial goals (goals within the next 10 years) that provide you with prosperity and a growth ladder.

When devising goals like these, you must keep your age in mind so that you do not financially struggle.

As you reach the age when you start to become completely independent, you unwillingly accept a lot of responsibility onto yourself. The biggest responsibility is keeping yourself financially stable.

These responsibilities will spontaneously originate more financial goals that will most likely be achieved within 10 years. The most common examples are buying/renting a house, financing your education, investing in acquiring additional skills that make you more inclined to getting hired, getting your own insurance, purchasing your own car, paying bills, etc.

To make it easier for you to achieve these financial goals, you must ensure that you are financially stable. Oftentimes, we may think we are financially stable; however, we do not realize that our current money habits may result in a negative impact in the far future.

You can prevent yourself from suffering in the future by making a financial plan that accounts for your current situation, financial goals, and possible future events.

Going back to how age impacts your financial goals, an elderly person’s financial plan will be specialized to support and incorporate retirement, medical bills, the decision to sell your property or distribute it among your loved ones, etc.

Important Steps in Creating a Financial Plan

Now that you have a better understanding of financial plans and how they are devised, you will now learn some of the most important steps in creating a successful financial plan.

1. Prepare a Detailed Sheet of Your Earnings and Expenses

One must start by identifying all possible streams of income and all expenses for one month. It is best to record your income and expenses every month because it is very likely that they constantly change.

For instance, if you know that you’re going to purchase the new iPhone being released next month, it is imperative that you include this expense in your financial plan. However, you’re not going to purchase a new phone every month, which is why you need your financial plan to be updated according to your income and expenses.

Furthermore, when taking note of your income and expenses, make sure to include dime.

To get you started, your income is ANY way you earn money: job, business, investing, commission, donations, etc. Expenses could be rent, food, electricity, water, travel, books, etc.

Do not leave out any detail thinking it’s too trivial to include. The best financial plans are created when every aspect is accounted for because it makes the plan more precise and accurate.

Apart from being more beneficial, doing this would also have the advantage of reliable records. These records could be used in the future as a reference as you can see how your income and expenses have evolved. You can use these statistics to compare, analyze, and better your financial plan.

For instance, if you know that you’re going to purchase the new iPhone being released next month, it is imperative that you include this expense in your financial plan. However, you’re not going to purchase a new phone every month, which is why you need your financial plan to be updated according to your income and expenses.

Furthermore, when taking note of your income and expenses, make sure to include dime.

To get you started, your income is ANY way you earn money: job, business, investing, commission, donations, etc. Expenses could be rent, food, electricity, water, travel, books, etc.

Do not leave out any detail thinking it’s too trivial to include. The best financial plans are created when every aspect is accounted for because it makes the plan more precise and accurate.

Apart from being more beneficial, doing this would also have the advantage of reliable records. These records could be used in the future as a reference as you can see how your income and expenses have evolved. You can use these statistics to compare, analyze, and better your financial plan.

2. Make a List of All Your Financial Goals

“Great things are done by a series of small things brought together” – Vincent Van Gogh

Do you want to be great? Do you want your financial condition to be great? If so, then take all those ambitions, goals, desires, and dreams, and put them together to create something better than you ever imagined.

The first step is to peacefully sit down and think of everything you want, regardless of how facile or difficult it is to achieve. Whatever you think of are your goals, some of which will be short-term while some will be long-term.

Some examples of short-term goals are paying the bills, purchasing a new laptop, etc. Short-term goals are anything that you want to achieve soon. Be aware of the fact that it must be achievable in a short period of time as well. For instance, you most likely can’t grow your income by a million dollars within 2 months.

Also, remember that as you progress, you will get additional short-term financial goals. As more goals originate, you must modify your financial plan so that your new goals will also be worked towards.

Meanwhile, long-term financial goals usually tend to take at least 5 years to realistically be achieved. These could include paying off a loan, growing a business to a global level, saving for retirement, etc.

Once you recognize what your financial goals are, the planning process begins.

Typically, your financial plan will mainly be specialized to alleviate the difficulty you experience when attempting to achieve your short-term goals, but will also ensure that you do not take any steps that will ultimately make it harder for you to achieve your long-term goals.

Regardless of your short-term goals, most financial plans will require you to save a portion of your earnings for emergencies and long-term goals.

For example, if your house bills are $1,000 per month, your financial plan might require you to allot $1,025 to your house bills so that you are prepared for an emergency, such as a window breaking.

Although $25 will not be sufficient to repair a window, your house bill savings from the previous months will most likely cover the expenses without complications.

Do you want to be great? Do you want your financial condition to be great? If so, then take all those ambitions, goals, desires, and dreams, and put them together to create something better than you ever imagined.

The first step is to peacefully sit down and think of everything you want, regardless of how facile or difficult it is to achieve. Whatever you think of are your goals, some of which will be short-term while some will be long-term.

Some examples of short-term goals are paying the bills, purchasing a new laptop, etc. Short-term goals are anything that you want to achieve soon. Be aware of the fact that it must be achievable in a short period of time as well. For instance, you most likely can’t grow your income by a million dollars within 2 months.

Also, remember that as you progress, you will get additional short-term financial goals. As more goals originate, you must modify your financial plan so that your new goals will also be worked towards.

Meanwhile, long-term financial goals usually tend to take at least 5 years to realistically be achieved. These could include paying off a loan, growing a business to a global level, saving for retirement, etc.

Once you recognize what your financial goals are, the planning process begins.

Typically, your financial plan will mainly be specialized to alleviate the difficulty you experience when attempting to achieve your short-term goals, but will also ensure that you do not take any steps that will ultimately make it harder for you to achieve your long-term goals.

Regardless of your short-term goals, most financial plans will require you to save a portion of your earnings for emergencies and long-term goals.

For example, if your house bills are $1,000 per month, your financial plan might require you to allot $1,025 to your house bills so that you are prepared for an emergency, such as a window breaking.

Although $25 will not be sufficient to repair a window, your house bill savings from the previous months will most likely cover the expenses without complications.

3. Budget Plan

If you are reading this article, you most likely have a budget that limits you from buying everything you lay your eyes on. If you have trouble with managing an effective budget, a budget plan will prove to be especially beneficial to you.

Now, even if you don’t have difficulty in managing a budget, you still need to create a budget plan to include in your financial plan.

A budget plan is the part of the financial plan that estimates potential expenses and savings based solely on earnings.

A budget plan will allow you to compare your actual expenses with the budgeted expenses, hence helping you understand cases of overspending/savings. In other words, it will control you from overspending because you will immediately know what the consequences will be if you do not follow your budget.

Furthermore, you clearly see and realize how much money you would save if you didn’t spend it on unnecessary products.

If this concept is ambiguous to you, or if you are unsure about whether or not a budget plan will be profitable for you, look at the example below.

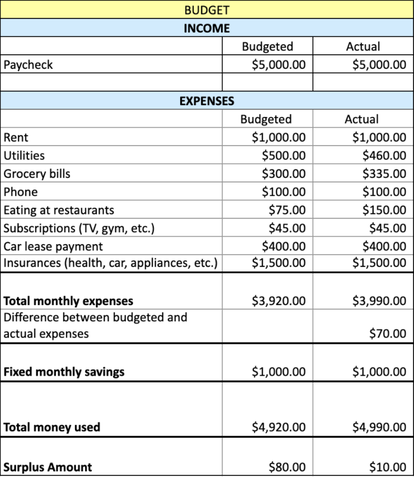

It is a simple personal budget for a period of 1 month. It depicts an exceedingly easy but useful way of how you can prepare a chart of your actual expenses compared to your budgeted expenses.

Now, even if you don’t have difficulty in managing a budget, you still need to create a budget plan to include in your financial plan.

A budget plan is the part of the financial plan that estimates potential expenses and savings based solely on earnings.

A budget plan will allow you to compare your actual expenses with the budgeted expenses, hence helping you understand cases of overspending/savings. In other words, it will control you from overspending because you will immediately know what the consequences will be if you do not follow your budget.

Furthermore, you clearly see and realize how much money you would save if you didn’t spend it on unnecessary products.

If this concept is ambiguous to you, or if you are unsure about whether or not a budget plan will be profitable for you, look at the example below.

It is a simple personal budget for a period of 1 month. It depicts an exceedingly easy but useful way of how you can prepare a chart of your actual expenses compared to your budgeted expenses.

In this budget, we can see that a fixed amount of $1,000 has been allocated for savings every month. Furthermore, the actual expenses are higher than the budgeted expenses, which is usually what always happens. For this reason, your budget will usually always spare some extra money.

In the plan above, the user is provided with a $80 surplus, which can either be used for emergencies, savings, or purchasing items he/she wants. The user ended up using $70 of those $80, leaving him with only $10.

Since he has already saved $1,000, the best decision would be to invest that $10. Although it may seem very less, small investments can be worth a fortune, if invested properly.

Furthermore, the $1,000 that he saved are meant to help him achieve his long-term financial goals.

Finally, this budget depicts how tight the budget is, and therefore, the user will be less likely to waste money, preventing him from debt. Looking at his budget, the user knows how careful he has to be with his spending habits if he wants to avoid debt.

Meanwhile, if he did not have a budget incorporated into his financial plan, he would be less aware of how much he spends.

To learn about the 4 types of budgeting methods, click here.

In the plan above, the user is provided with a $80 surplus, which can either be used for emergencies, savings, or purchasing items he/she wants. The user ended up using $70 of those $80, leaving him with only $10.

Since he has already saved $1,000, the best decision would be to invest that $10. Although it may seem very less, small investments can be worth a fortune, if invested properly.

Furthermore, the $1,000 that he saved are meant to help him achieve his long-term financial goals.

Finally, this budget depicts how tight the budget is, and therefore, the user will be less likely to waste money, preventing him from debt. Looking at his budget, the user knows how careful he has to be with his spending habits if he wants to avoid debt.

Meanwhile, if he did not have a budget incorporated into his financial plan, he would be less aware of how much he spends.

To learn about the 4 types of budgeting methods, click here.

4. Make Wise Investments

Saving small amounts out of your earnings on a periodical basis, such as monthly or quarterly, helps accumulate funds. To make the most out of these funds, you need to invest.

Note: This article has already discussed why investing is so important when developing a financial plan.

Some options of investing are listed below:

Note: before you start investing you must learn how to invest so that you lose as little money as possible. Additionally, NEVER invest all of your excess funds. If you invest everything, you are risking a large amount of your wealth.

Also, if you invest everything, you will be more inclined to spend it rather than save it for your long-term financial goals, such as retirement.

Note: This article has already discussed why investing is so important when developing a financial plan.

Some options of investing are listed below:

- Invest in stocks and company bonds, with a mix of funds in both areas. This will help to balance the losses (if any) with the gains made.

- Keeping some funds in deposits with your bank that can earn a higher rate of interest after a period of time.

- Purchase of gold that has an appreciation value with time can fetch a higher valuation when sold. The gold rate constantly fluctuates, hence, you can sell the gold once the value rises above your purchase value.

Note: before you start investing you must learn how to invest so that you lose as little money as possible. Additionally, NEVER invest all of your excess funds. If you invest everything, you are risking a large amount of your wealth.

Also, if you invest everything, you will be more inclined to spend it rather than save it for your long-term financial goals, such as retirement.

5. Credit Card Management

A responsible and timely attitude will go a long way in reducing unnecessary late fees and other charges in maintaining your credit card usage.

Your financial plan will allow you to take various financial actions, such as getting a loan, when your credit card score is high.

Apart from this, paying your bills on time will allow you to continue as per your financial plan without paying late fees.

Adhering to the following advice will be worthwhile for a better financial state.

Your financial plan will allow you to take various financial actions, such as getting a loan, when your credit card score is high.

Apart from this, paying your bills on time will allow you to continue as per your financial plan without paying late fees.

Adhering to the following advice will be worthwhile for a better financial state.

- Pay for daily-use items or groceries in cash.

- Pay the credit card bills on time, hampering your credit card score.

- Try not to spend beyond the budgeted expense limit.

- Practice restraint in using your credit card on expensive items because you do not know much you are spending. Since you cannot directly see your bank account when using a credit card, you will not know much money you are spending. As a result, people frequently exceed the expenses limit their financial plan allows.

6. Have a Retirement Plan

Saving for your retirement is crucial in your financial planning because it allows you to comfortably live your retirement.

You can adjust your plan to suit your income and the funds needed for your retirement preferences. The different retirement preferences are discussed here.

Furthermore, your financial plan will also require you to decide where you want to keep your retirement savings. You can either keep your retirement savings in your bank account or in a retirement account (IRA), such as 401(k).

Keeping your savings in an IRA has benefits but also disadvantages. A benefit of an IRA is that it can reduce the amount of income tax you have to pay.

The disadvantage is that it limits your control over your money. For instance, you cannot withdraw money whenever you want to.

There are many more benefits and disadvantages of IRAs that you should consider before determining whether you want to keep your money in an IRA or in a bank account.

You can adjust your plan to suit your income and the funds needed for your retirement preferences. The different retirement preferences are discussed here.

Furthermore, your financial plan will also require you to decide where you want to keep your retirement savings. You can either keep your retirement savings in your bank account or in a retirement account (IRA), such as 401(k).

Keeping your savings in an IRA has benefits but also disadvantages. A benefit of an IRA is that it can reduce the amount of income tax you have to pay.

The disadvantage is that it limits your control over your money. For instance, you cannot withdraw money whenever you want to.

There are many more benefits and disadvantages of IRAs that you should consider before determining whether you want to keep your money in an IRA or in a bank account.

Conclusion

Now that you have read this article, you should have a strong understanding of how to devise the financial plan. By taking the above information, you can write a financial plan that best accommodates your preferences.

Once you fully comprehend all the tips and information stated in this article, your financial plan will turn out to help you in so many ways you didn’t ever imagine.

Once you fully comprehend all the tips and information stated in this article, your financial plan will turn out to help you in so many ways you didn’t ever imagine.

Contact Us With Any Questions or Comments

Continue learning by reading our other articles.

Works Cited

“Personal Finance.” Corporatefinanceinstitute.com, CFI Education Inc.,

https://corporatefinanceinstitute.com/resources/knowledge/finance/personal-finance.

Voigt, Kevin and Alana Benson. “What is a financial plan, and How Can I Make One?” nerdwallet.com, Nerdwallet, Inc, Aug.4, 2021,

https://www.nerdwallet.com/article/investing/what-is-a-financial-plan.

Kenton. Will. “Personal Finance.” Investopedia, Dotdash, March 30,2021,

https://www.investopedia.com/terms/p/personalfinance.asp#personal-finance-principles

Fried, Carla. “Personal Finance 101: The complete guide to managing your money.” CNBC.com, CNBC LLC, Jan. 12, 2021, https://www.cnbc.com/guide/personal-finance-101-the-complete-guide-to-managing-your-money

https://corporatefinanceinstitute.com/resources/knowledge/finance/personal-finance.

Voigt, Kevin and Alana Benson. “What is a financial plan, and How Can I Make One?” nerdwallet.com, Nerdwallet, Inc, Aug.4, 2021,

https://www.nerdwallet.com/article/investing/what-is-a-financial-plan.

Kenton. Will. “Personal Finance.” Investopedia, Dotdash, March 30,2021,

https://www.investopedia.com/terms/p/personalfinance.asp#personal-finance-principles

Fried, Carla. “Personal Finance 101: The complete guide to managing your money.” CNBC.com, CNBC LLC, Jan. 12, 2021, https://www.cnbc.com/guide/personal-finance-101-the-complete-guide-to-managing-your-money